News

W15 2025: Sunflower Oil Weekly Update

Original content

1. Weekly News

Global

Global Sunflower Oil Market Faces Weak Demand Despite Stable Supply

Sunflower oil losing market share in global consumption, there will be no global sunflower seed shortage by the end of the season. Inventories in key Black Sea producing countries remain at last year's levels, yet demand has significantly decreased due to a widened price spread between sunflower oil and other vegetable oils. Key price drivers include the Russian ruble's exchange rate, farmer sentiment, and weather.

Bulgaria

Bulgaria's Oilseed Industry Faces Crisis Amid Sunflower Shortage

Bulgaria's oilseed processing industry is facing a crisis due to a severe shortage of raw materials, according to the administrative director at trading company Oliva AD’s facility in Razdelna. While the country’s processing capacity is around 4 million tons of sunflower annually, domestic production yields only about 2 million tons. Previously covered by imports, the gap has widened due to licensing issues with Ukrainian deliveries. Compounding the problem, last year’s domestic sunflower harvest was both low in volume and quality. To adapt, processors have turned to alternative oilseeds, notably importing 314,000 tons of rapeseed this year—including a major shipment of 58,300 tons from Canada.

European Union

EU Oilseed Processing Drops to 3-Year Low Amid Market Instability

In the first two months of the year, oilseed processing volumes for the EU crops fell by 8% year-on-year (YoY) to 8 million tons—the lowest level in three years. Soybean and sunflower processing saw the sharpest declines, each dropping 20% to 2.62 million and 1.30 million tons, respectively, with notable decreases in France, Bulgaria, Romania, Poland, and Hungary. Rapeseed processing also contracted by over 8% to 4.07 million tons. The market drop is attributed to the market volatility and reduced product demand but suggest that a recovery may occur in the second half of the year if prices stabilize and processing interest rises.

Russia

Russia’s Vegetable Oil Exports Plunge Amid Unprofitability and Policy Pressures

In Q1-2025, Russia’s vegetable oil exports dropped by 27% YoY, with sunflower oil exports falling by 38%, primarily due to rising raw material costs, high export duties, and a stronger ruble reducing global competitiveness. Processing volumes shrank by 20%, while sunflower oil export profitability turned negative, contrasting with strong Q4-2024 performance. A spike in domestic sunflower seed prices outpaced export price gains, triggering higher duties and further straining margins. Despite the downturn, rapeseed oil exports surged by 29% thanks to Chinese demand amid Canadian import tariffs. Without regulatory adjustments, the market outlook remains bleak.

Sunflower Oil Output in Krasnodar Region Surges by 20% in 2024

In 2024, Russia’s Krasnodar region boosted vegetable oil production by 10% YoY to 1.26 million metric tons (mmt). This is driven mainly by a 20% rise in sunflower oil output, which reached 1.098 mmt—nearly 90% of the region’s total. Soybean oil production also grew by 23% to 52,400 mmt. With over 50 processing enterprises and a combined sunflower crushing capacity of 3 mmt annually, the region now accounts for more than 20% of Russia’s total vegetable oil output. Products are sold domestically and exported to China, Georgia, and Turkey. Ongoing investment projects are modernizing production capacity further.

Ukraine

Western Ukraine Found Unsuitable for Sunflower Cultivation

Sunflower cultivation in western Ukraine is largely unsuccessful due to high humidity and resulting plant diseases, according to the owner of Agrarian Technological Company. He argues that sunflower trials in the region consistently fail under normal weather conditions and only perform marginally better during drought years. He warns against building oil extraction plants in the west, calling it a major mistake due to insufficient raw material supply, which could lead to losses instead of profits. He recommends soybean and rapeseed processing instead, if economically justified, based on the hydrotechnical coefficient (HTC), which helps determine suitable crop zones: higher HTC favors soybeans, while lower HTC is better for sunflowers.

2. Weekly Pricing

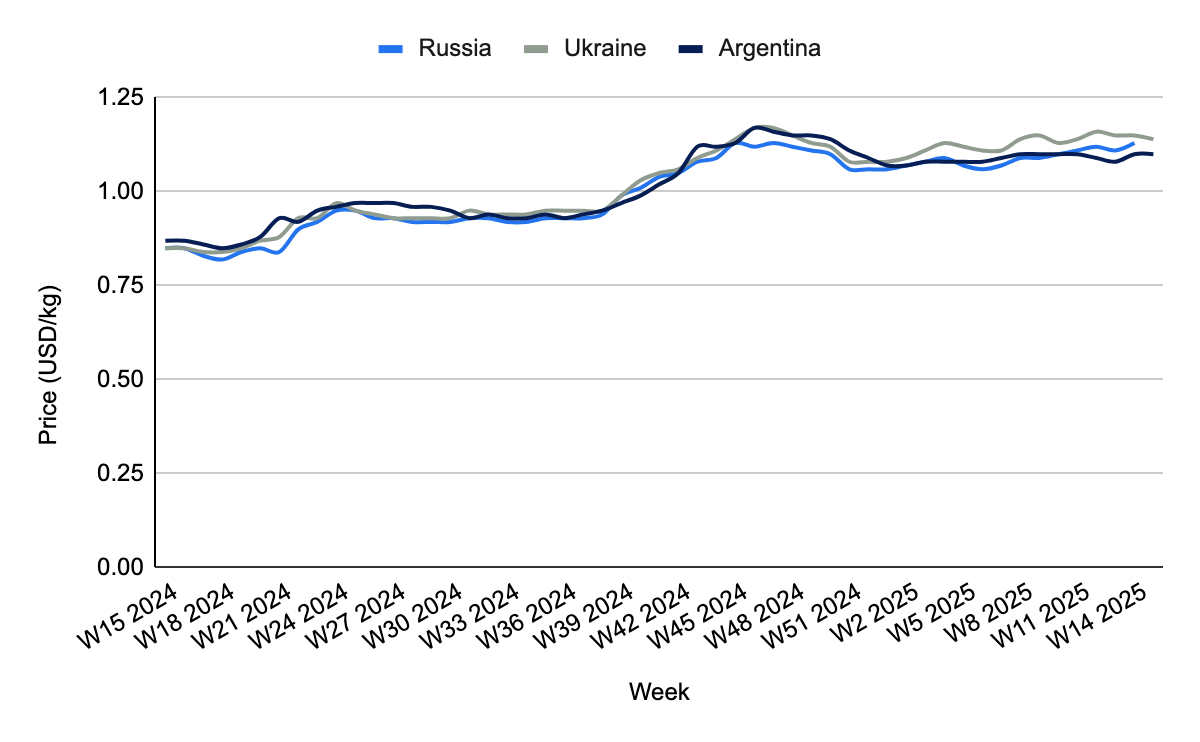

Weekly Sunflower Oil Pricing Top Producers (USD/kg)

_18.27.24.png)

Yearly Change in Sunflower Oil Pricing Top Producers (W15 2024 to W15 2025)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Ukraine

Sunflower oil prices in Ukraine recorded a WoW decline of 0.87% and a MoM drop of 1.72%, despite a notable YoY increase of 34.12% to USD 1.14 per kilogram (kg) in W15. The yearly rise reflects tighter domestic supply caused by reduced processing activity and limited cultivation capacity, particularly in the western region where high humidity and disease pressure hinder production. High demand for high-oil-content seeds and firm export interest had sustained elevated prices earlier. However, the recent WoW and MoM drops point to emerging bearish sentiment, driven by external macroeconomic pressures including declining crude oil prices, weaker United States (US) economic indicators, and increased oil output. These global factors have tempered buyer enthusiasm and triggered more cautious selling behavior, easing prices slightly despite the tighter long-term fundamentals.

Argentina

In W15, sunflower oil prices in Argentina remained stable at USD 1.10/kg, showing no change WoW, while prices rose slightly by 0.92% MoM and increased more substantially by 26.44% YoY. The unchanged weekly price reflects a momentary balance in market dynamics, with steady domestic availability and sustained export flows. The modest MoM growth points to persistent, but easing, upward pressure. In contrast, the strong YoY increase highlights Argentina’s growing importance in global sunflower oil trade, driven by favorable local supply conditions, expanded processing activity, and robust international demand. The country’s unique freight compensation system, which offsets logistical costs between production areas and processors, continues to shape price-setting strategies. With Ukraine and the EU facing production constraints, Argentina’s export competitiveness remains firm, keeping prices resilient over the longer term.

3. Actionable Recommendations

Capitalize on Brazil's Tariff Cuts to Expand EU Export Reach

EU producers, especially from Portugal, Spain, and Italy, should aggressively expand their sunflower oil exports to Brazil following the removal of import tariffs. With olive oil already demonstrating robust demand and consumption growing fourfold over the past two decades, sunflower oil exporters can tap into this liberalized market by highlighting their oil's health benefits and competitive pricing. Strategic partnerships with Brazilian importers and major retail chains, combined with localized marketing efforts promoting European origin and quality, can quickly increase shelf space and build brand recognition. The move also supports long-term positioning ahead of broader EU-Brazil free trade agreements, allowing for sustained competitive access.

Target Argentina for Long-Term Supply Security and Trade Growth

Importers in markets affected by supply volatility in Ukraine and Russia should increasingly source sunflower oil from Argentina. The country’s growing role in global trade, supported by strong domestic supply, an efficient freight compensation system, and steady processing expansion, offers a reliable alternative. Buyers should secure medium- to long-term contracts with Argentine exporters to lock in favorable prices and mitigate risk. Additionally, trade promotion agencies can support partnerships through bilateral trade facilitation, technical support on certifications, and joint ventures in storage and port logistics, improving overall trade resilience.

Reassess Bulgaria and EU Processing Strategies Amid Declining Volumes

Processors and traders in the EU, especially in countries like Bulgaria, Romania, and Hungary, need to adapt to a multi-year low in oilseed crushing by recalibrating capacity use and diversifying input sourcing. Bulgaria's crisis, caused by a domestic shortfall and import licensing delays, highlights the need for a flexible raw material procurement strategy. Processors should increase short-term rapeseed imports, as already seen with Canadian shipments, and explore oilseed alternatives like soybeans. For EU-wide stakeholders, investment in processing flexibility (multi-seed crush plants) and harmonized import procedures will reduce bottlenecks and increase resilience in future market disruptions.

Sources: Tridge, Agro Portal UA, Grain Trade, Milk News, Sinor BG, Super Agronom, UKR Agro Consult, Vina Net

Read more relevant content

Recommended suppliers for you

What to read next