OPINIO

Original content

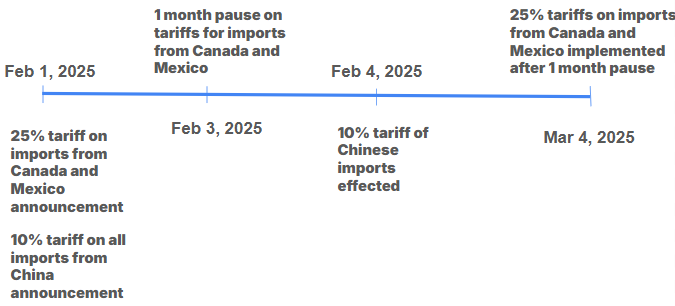

In early 2025, the United States (US) administration under President Donald Trump implemented significant tariff measures affecting imports from Canada, Mexico, and China. Aimed at addressing trade imbalances and protecting domestic industries, these actions have had severe implications for the US agricultural sector.

February 1, 2025: The US President signed executive orders imposing a 25% tariff on all imports from Canada and Mexico, with Canadian energy resources subject to a reduced 10% tariff. Additionally, a 10% tariff was imposed on all imports from China. These tariffs were initially set to take effect on February 4, 2025.

February 3, 2025: The US announced a one-month pause on the tariffs for Canada and Mexico after these countries agreed to enhance border enforcement measures. Consequently, the tariffs on Canadian and Mexican imports were delayed until March 4, 2025.

February 4, 2025: The 10% tariff on Chinese imports came into effect as scheduled.

March 4, 2025: The 25% tariffs on imports from Canada and Mexico were implemented following the expiration of the one-month pause.

Figure 1: Chronology of Tariffs Imposed by the US government on Canada, Mexico, and China in 2025

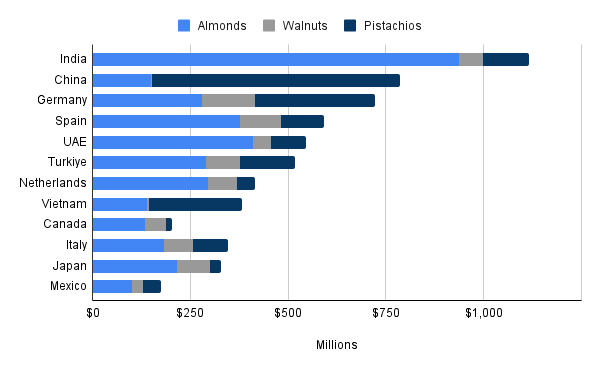

It is expected that China, Canada, and Mexico could impose retaliatory tariffs following the import tariffs imposed by the US on all three nations. Such retaliatory measures could impact US nut exports as China, Canada, and Mexico remain significant markets. According to the ITC Trade Map, in 2024, the three nations ranked as the 2nd, 9th, and 12th largest export destinations for US nut exports (HS Code: 0802), respectively. Regarding nut varieties, almonds make up nearly 70% of the US tree nut export volume, with walnuts and pistachios contributing over 10% and 9%, respectively. Therefore, any retaliatory tariffs from China, Canada, and Mexico would primarily affect these three nut varieties.

Figure 2: 2024 US Nut Exports to Leading Destinations in 2024

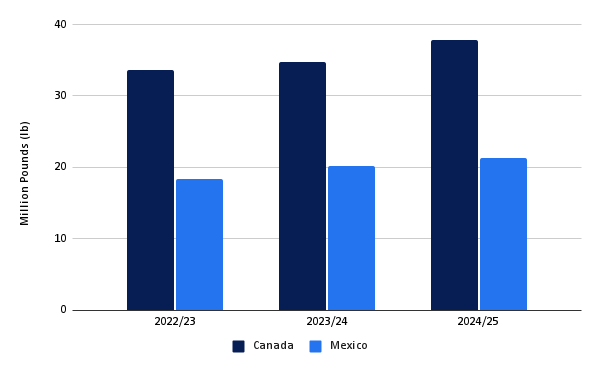

According to the Almond Board of California, recent shipment data highlights the US’ growing dependency on the Canadian and Mexican markets, with total shipments for 2024/25 Year-to-Date (YTD) reaching 37.79 million pounds (lb) and 21.35 million lbs, a 12.3% and 16% increase over the past three years, respectively. This outlines the growing significance of these markets to US almonds suppliers and underlines how impactful the tariffs could be.

Figure 3: Total Shipments of US Almonds (YTD)

This situation could lead to retaliatory tariffs from both countries leading to two main outcomes; an oversupply in the US domestic market, potentially driving prices down and Chinese, Canadian and Mexican importers seeking out alternative suppliers. Both these outcomes could result in diminished profit margins for US producers. However, deeper analysis shows that both outcomes could have a limited impact on prices and trade.

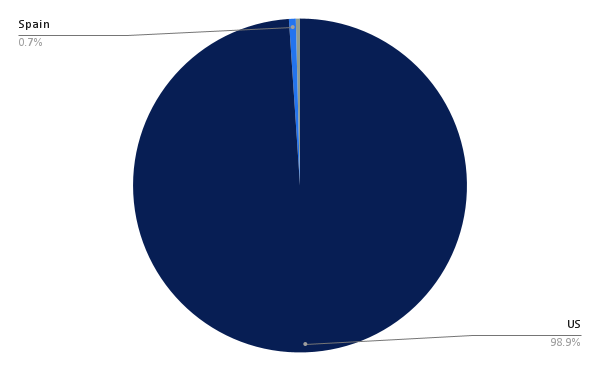

Firstly, retaliatory tariffs would not significantly alter Canadian almond trade. It is highly unlikely that Canadian importers would shift from sourcing US almonds as the US commands a large share of the Canadian market. According to the ITC Trade Map, Canada imported USD 138.04 million worth of almonds, shelled and in shell, in 2024, with USD 135.70 million originating from the US, resulting in a market share of 98.3%. That being said, Spain, accounting for 1% of the Canadian almond market, could witness slight gains but the US is set to remain Canada's main source of almonds, owing to its close proximity and high quality almonds. The case is also similar in Mexico, where all of its USD 23.24 million worth of almond imports, shelled and in shell, originated from the US in 2024, highlighting the lack of significant competitors to the US in both markets.

Figure 4: Percentage of Canadian Almond (shelled and in shell) Imports Between Top 3 Countries of Origin (the US, Spain and Afghanistan)

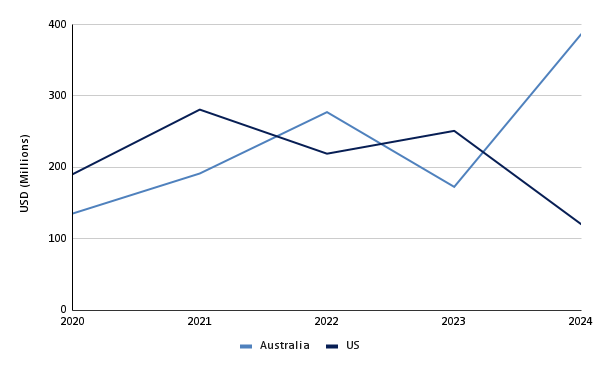

However, the situation is different when it comes to China. If China imposes retaliatory tariffs on US imports, US almond suppliers could lose ground in the Chinese market as China is transitioning from its previous dependence on US almonds towards Australian almonds. According to the ITC Trade Map, China imported USD 120.03 million worth of US almonds, shelled and in shell, in 2024, a significant 51.2% year-on-year (YoY) decrease. On the other hand, China imported USD 386.94 million worth of Australian almonds, shelled and in shell, in the same year, a notable 124.2% YoY increase. As a result, retaliatory tariffs on US imports could lead to Chinese importers opting for Australian almonds, further reducing the US’ market share in China.

Figure 5: Chinese Imports of Almonds (shelled and in shell)

Regarding prices, the US Bureau of Labor Statistics Producer Price Index for almonds has held steady at 357.337 since Apr-24. However, a notable drop in the index is expected if China imposes retaliatory tariffs on US products, as an increase in US domestic supply could result in a bearish price trend.

Retaliatory tariffs would impact US walnut suppliers significantly in the Chinese market. The case here is similar to that of almonds, with China transitioning away from US walnuts (shelled) toward Australian walnuts (shelled). In 2024, China imported USD 323,000 worth of US walnuts (shelled), a notable 40.5% YoY decrease, while imports of Australian walnuts (shelled) amounted to USD 204,000, a significant increase of 158.2% over the past two years. As a result, retaliatory tariffs would suit Australian walnuts (shelled), allowing them to become cheaper and more competitive in the Chinese market than US walnuts (shelled).

Similarly, the US faces stiff competition from Chile and Kyrgyzstan in the Chinese market regarding walnuts (in shell). Between 2020 and 2023, Chile dominated the market, with a market share of 95.1% compared to the US’ 4.9%. Additionally, US exports of walnuts (in shell) to China have dwindled from USD 3.11 million in 2020 to USD 0.3 million in 2023, a significant 90.2% drop as China continues to relinquish its dependence on US products. Therefore, if retaliatory tariffs are passed, Chile would pose the greatest threat to the US in the Chinese market. Furthermore, the emergence of Kyrgyzstan as a major player in 2024 is a cause for concern for US walnut (in shell) suppliers. Kyrgyzstan exported USD 2.44 million worth of walnuts (in shell) in 2024, eclipsing the US’ USD 1.17 million and rivalling Chile’s USD 3.24 million. This was the first time Kyrgyzstan had entered the Chinese market and it is yet to be seen if this momentum will be sustained in 2025.

Despite this trend, Chinese imports of US walnuts, both in shell and shelled, are quite insignificant with China making up only 0.3% (USD 3.14 million) of the US’ total exports (USD 1.09 billion). Therefore any losses in the Chinese market would not greatly impact the US’ overall walnut exports.

Additionally, retaliatory measures from Canada and Mexico will have limited impact as they are both heavily reliant on US walnuts. According to the ITC Trade Map, Canadian imports of US walnuts, both shelled and in shell, amounted to USD 62.01 million in 2024, with USD 58.81 million (94.8%) originating from the US. Similarly, Mexican imports of US walnuts, both shelled and in shell, amounted to USD 75.62 million, with 100% originating from the US.

Pistachio producers face similar challenges. Increased tariffs on exports to major markets such as China could lead to reduced demand for US pistachios, allowing competitors from countries like Iran and Turkey to capture a larger share of the market. In 2024, China imported USD 6.19 million worth of pistachios (shelled) from the US, with a similar amount of USD 6.06 million imported from Iran. Additionally, Chinese imports of Iranian pistachios (shelled) have grown by 150% over the past year, surpassing the 71.5% yearly increase in US pistachio (shelled) imports. This trend highlights the growing demand of Iranian pistachios (shelled), which would be heightened by any retaliatory tariffs imposed on US imports to China. This shift could result in decreased revenues for US producers and necessitate strategic adjustments to maintain global competitiveness.

The case is somewhat different regarding Chinese imports of pistachios (in shell). In 2024, China imported USD 578.24 million worth of pistachios (in shell) from the US, and only USD 262.41 million from Iran. The gap between the countries of origin is far greater in this regard with the US commanding 64.5% of the market share, while Iran accounts for 30.6%. Retaliatory tariffs could be less impactful in this case owing to the US’ market dominance. Iran could still benefit and increase its market share in China, however, the impact is significantly lower for pistachios (in shell) than it is for pistachios (shelled).

US pistachio suppliers will need to focus more on major markets in the European Union (EU), such as Italy and Germany. In both these countries, demand for US pistachios, both shelled and in shell, has scaled significantly in recent years. In 2024, Italy imported USD 32.63 million worth of pistachios (shelled) from the US, a 61.77% YoY increase. Similarly, Germany imported USD 32.07 million worth of pistachios (shelled) from the US, a 92.5% YoY increase. The case is similar for pistachios (in shell). Germany imported USD 262.88 million worth of US pistachios (in shell) in 2024, a 58.9% YoY increase, with Spain importing USD 106.06 million worth of US pistachios (in shell), 5.3% more than the previous year. As a result, greater focus on these markets could prove profitable for US suppliers.

Considering the data discussed above, it is clear that retaliatory tariffs from Canada and Mexico would not significantly hamper US nut exports, especially regarding the leading nut varieties; almonds, walnuts, and pistachios. Firstly, Canada and Mexico are dependent on the US for the supply of nuts, particularly Mexico, which imports all its almonds and walnuts from the US, with no other competing country of origin, with Spain a distant competitor for the US in the Canadian market. As a result, the implementation of retaliatory tariffs will not affect US nut exports to these destinations.

However, these tariffs would result in US nuts becoming significantly more expensive for Canadian and Mexican importers. For example, if we consider the case of almonds. In 2023/24, the average unit price of US almonds (shelled) imported into Canada and Mexico was USD 4,927 per metric ton and USD 4,942/mt, respectively. If both nations were to impose a retaliatory tariff of 25%, import prices of almonds into Canada and Mexico would rise to approximately USD 6,158.75/mt and USD 6,177.50/mt, respectively. Such a rise in costs would be significant and would see Canadian and Mexican importers and retailers pass this cost down the supply chain to the end user, making nuts notably more expensive.

The case is somewhat different for China. China is not as dependent on US nuts as Canada and Mexico are and has been transitioning towards other countries of origin, such as Australia and Iran. Therefore, the Asian nation could impose retaliatory tariffs and turn to other countries of origin, squeezing the US out of the Chinese market. However, the quantities imported by China are insignificant and would not greatly affect US nut exports. To compensate for the potential loss of market share in China, US producers will need to focus on key and growing markets, especially in Europe, such as Spain, Turkiye, Italy, and Germany to avoid potential losses, and develop new strategies to remain competitive as the trade environment changes.

Tools such as Tridge Eye can help nut suppliers and buyers make strategic decisions to navigate the current US tariff situation utilizing AI powered intelligence.

Read more relevant content

Recommended suppliers for you

What to read next